Significant shareholders who want out

Significant shareholders who want out

5 large investors who we think want to bail

Shareholder overhang is a term often heard. Stocks that are illiquid tend to trade at lower multiples than more liquid peers. Larger controlling insiders can be seen at times as a threat, deterring other institutions or funds from taking a position. In some cases, under the right circumstances, a significant stake may be beneficial to smaller unitholders where they press management to unlock value either thru an activist approach or sale and we think some examples of that exist today.

In this article, we will quickly explore and identify 5 different energy names where a significant insider controls a large swath of shares. In the first three, we think it will be a negative and common investors are likely to suffer; in two smaller and lesser known OFS service names, we will discuss why we think it is a positive and how shareholders may maximize value.

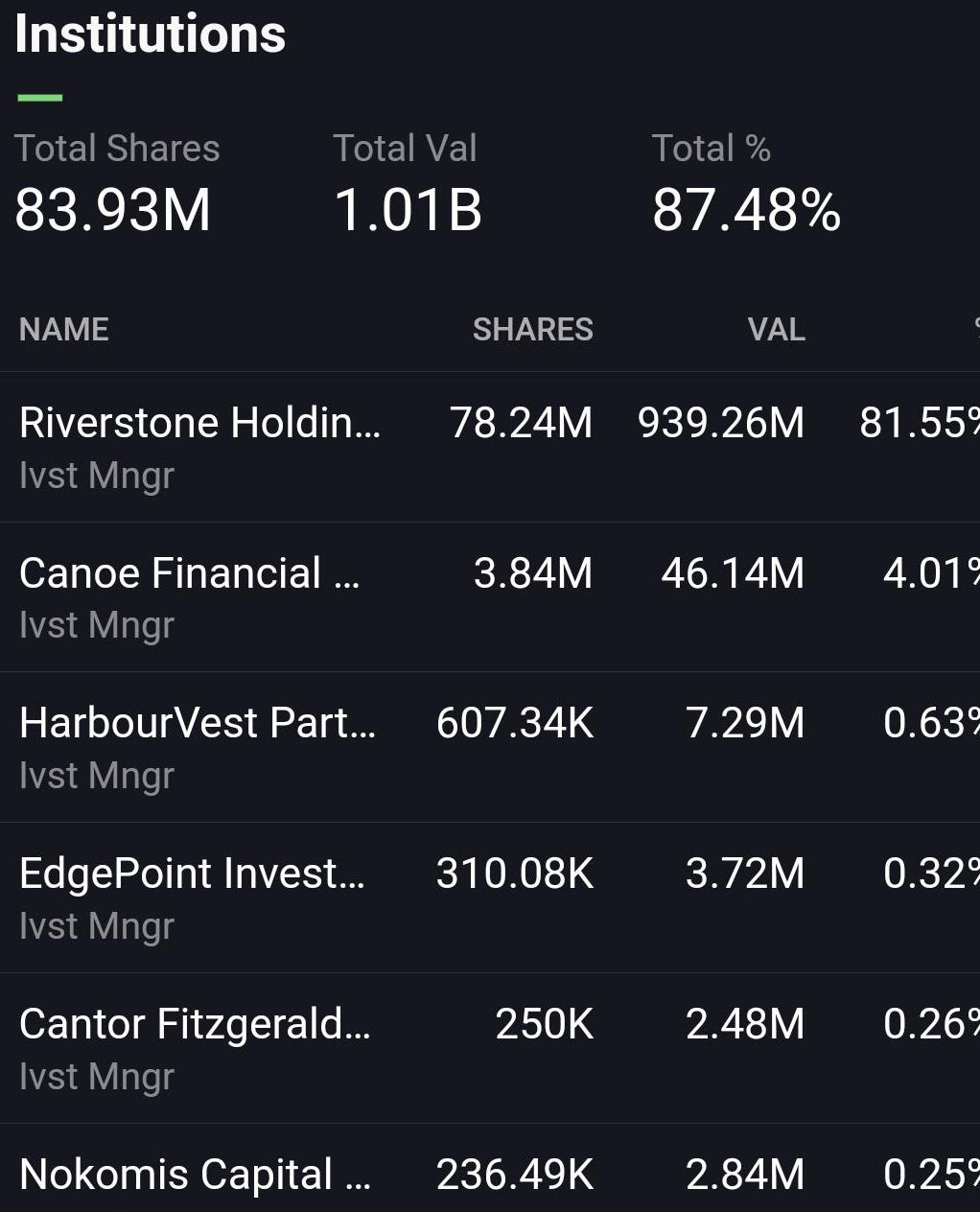

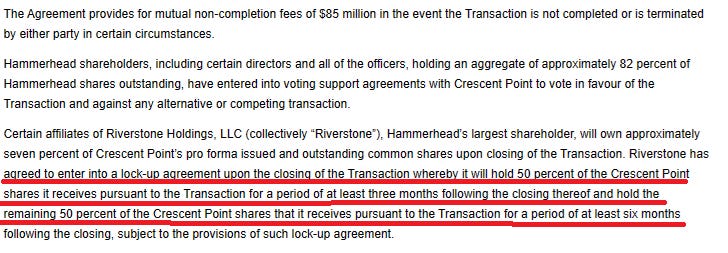

Crescent Point Energy (Significant shareholder: Riverstone)

With $1.6 billion dollars in Crescent Point stock held by Riverstone acquired through the recent Hammerhead Resources transaction, we don’t think they have much long-term ambition and will rather instead opt to liquidate as soon as reasonably possible on both tranches of shares. The amount held here is sizeable. With an already failed bought deal resulting in a hung deal on the original transaction, we think such an amount of shares on the market will test the resolve of retail investors for Crescent Point stock which we think will remain out of favour for some time. It’s logical to assume that Riverstone’s gradual liquidation of shares will result in overhang, casting a negative and short-term dark shadow over Crescent Point’s performance.

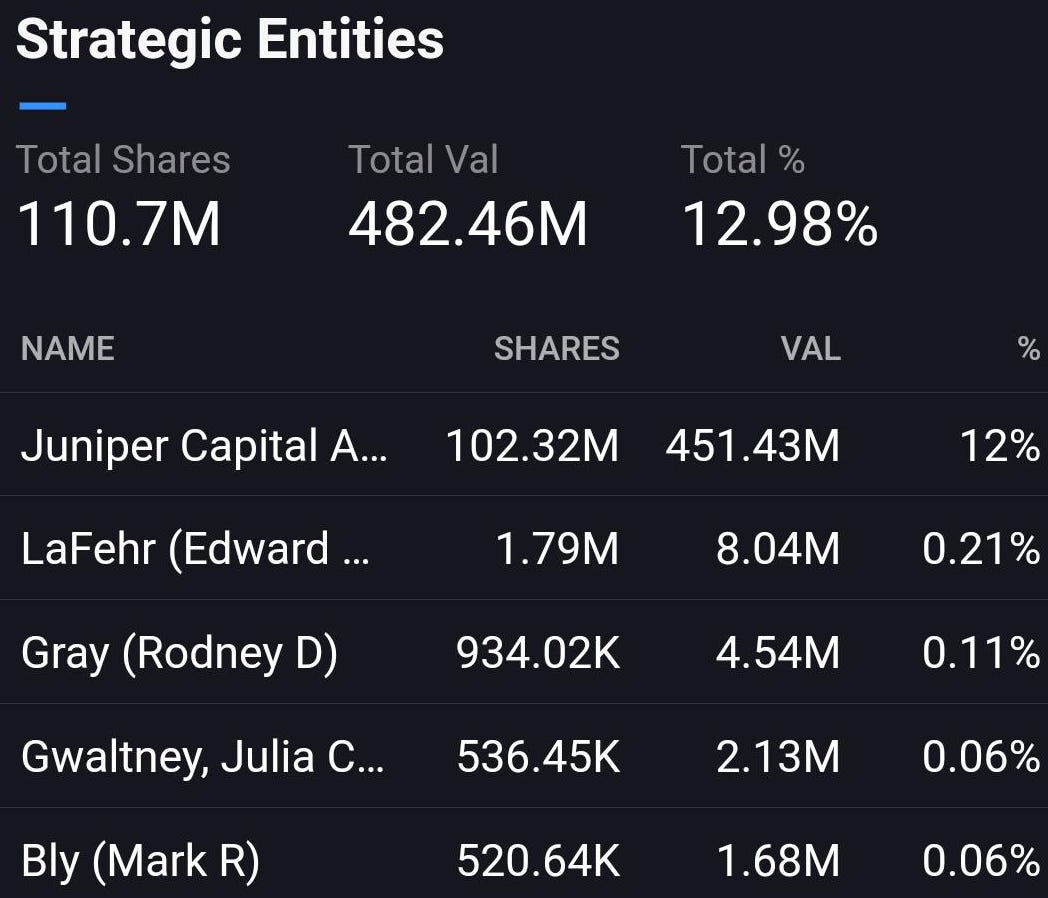

Baytex Energy (Significant shareholder: Juniper)

Juniper became Baytex’ largest shareholder earlier this year after the company acquired Eagleford rival Ranger Oil. After initially seeing a large sell off when the deal was announced, Baytex shares recovered a bit and the new largest shareholder was swift to sell their first tranche, liquidating 51.1 million shares on the market at $5.65. Given the stock is now down -23% since, we congratulate Juniper on their sale and we think that this private equity outfit will be swift to sell any meaningful rallies as it seems rather evident they want out of Baytex. We see the remaining overhang as a likely negative dark cloud over the stock that should lead to underperformance. It is reasonable to expect Juniper to use any ‘hot’ retail bids to market the next trench. With $451 million worth of Baytex shares, the impact is likely to felt by extended underperformance without a single large taker of shares.

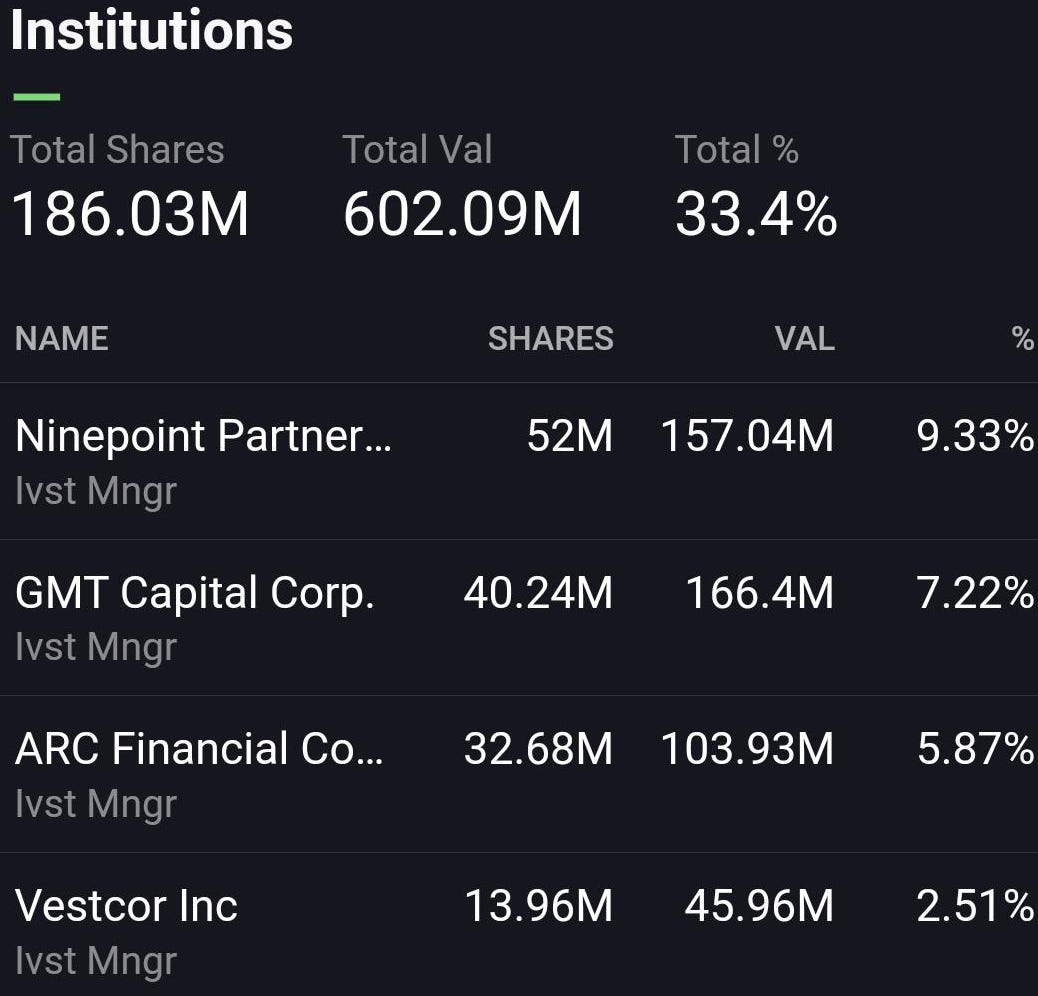

Tamarack Valley (Significant shareholder: Arc Financial)

Arc Financial became a large shareholder in Tamarack Valley in 2022 from the Deltastream Energy acquisition in the Clearwater. The company issued shares at $3.75, well above where they are trading today. Arc has a period of a 6-month & 12-month lock-up period as to disposition potential, and they wasted absolutely no time in selling the first trench as soon as they could earlier this year as the retail appetite for its stock was elevated given the constant touting on Marketcall and multiple sellside banks which were involved in the transactions. With the second and final trench of shares potentially available to hit the market anytime, Arc’s $103 million worth of shares should have less overhang but still enough to cast some clouds given energy is currently out of favor and Tamarack even more so.

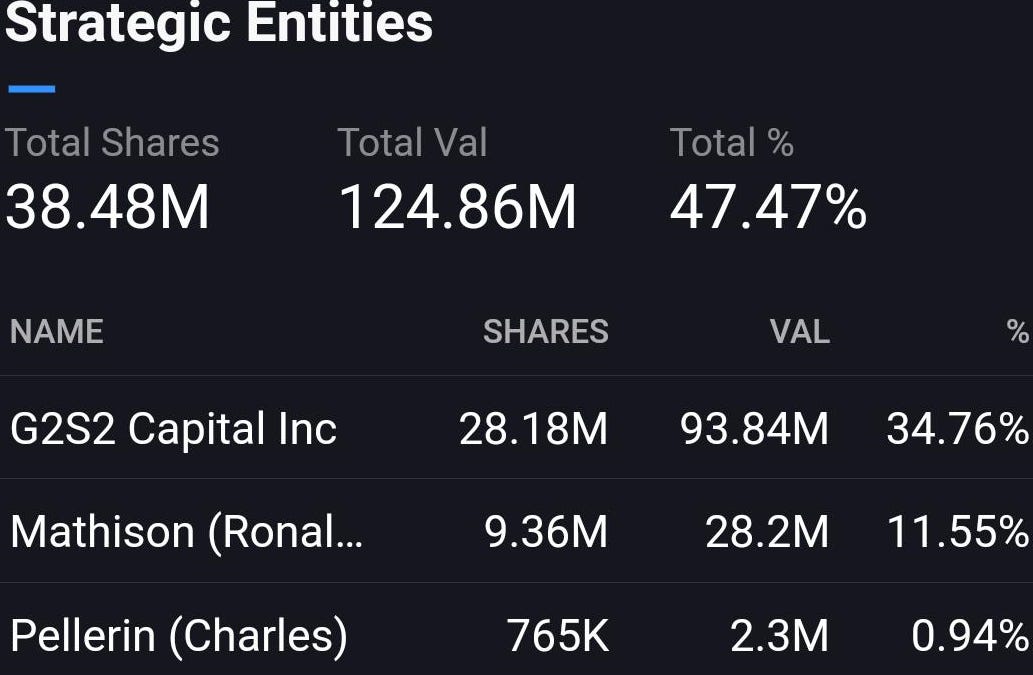

Calfrac Well Services (Significant shareholder: G2S2)

Calfrac Well Services is an oilfield service name that has been embroiled in multiple existential challenges over the past decade. In a nutshell, to get out of their last one that got them to where they are today, they had to make a deal with often activist investor George Armoyan and G2S2 who helped restructure the company. In doing so, his private equity firm became a commanding shareholder in the new Calfrac. Armoyan is now stuck in Calfrac for multiple years while waiting it out. With multiple recent M&A transactions in both U.S. and Canada, we think Calfrac could be sold in either country piece by piece. Our view is that Calfrac’s U.S. asset base would be liquid to numerous buyers in what is becoming an extremely consolidating frac market, where size and scale are imperative. Canada we are not so sure about but are leaving the door open to a potential merger between Calfrac & STEP. Calfrac also has assets in Argentina’s shale play which has picked up steam and think the company now has potential to dispose of assets there. Given an extremely low multiple on Calfrac, we think that any M&A transaction would have to be done at a decently higher trading price to where shares are valued at today to appease Armoyan & Mathison who are known to be patient and well capitalized investors. In this case we think Calfrac’s overhang is likely to become a positive.

Western Energy Group (Significant shareholder: G2S2)

G2S2 became a shareholder in Western Energy very much as they did thru Calfrac, as part of a restructuring process led by George Armoyan and AIMCO. Having been sitting in this name for a couple years we think G2S2 is likely getting impatient and would be keen to liquidate their stake. With recent smallcap OFS M&A picking up in Canada this year, we think there are likely a few possible buyers for Western Energy with the most likely outcome as Ensign or Total Energy Services. While we think it’s a take out candidate we also find it hard to get excited at this juncture given the name is more expensive relative to peers. Should activity levels pick up in Canada and where marketshare becomes a thorn in the side of larger competitors, it would be reasonable to expect Western Energy to be one of the first companies sold.

Thank you for reading our latest piece. We hope you enjoyed it and welcome your comments as we start a new phase in the economic cycle.

Yours truly,

Roger Lafontaine

Partner, Head Trader & Research Analyst, Nugget Capital Partners

| A guest post by

|

| A guest post by

|