Strathcona Resources, why it's still our top E&P pick into Q2 earnings.

Greetings friends,

I thought this morning I would write-up a short article about Strathcona Resources, the E&P that was our top pick for 2024 that we had Tweeted and Substacked numerous times about over the past year. Overall our views on Strathcona Resources have not changed and we have been impressed with how the team has executed since going public with the Pipestone Energy acquisition.

Despite being moderately bearish on oil and natural gas, as well as other commodities into what I believe in a macro slowdown led by China, I still think there are some near-term opportunities in the Canadian Energy space with Strathcona Resources continuing to feel like the most obvious one on a risk-reward and near-term basis.

Ultimately the outlook for Canadian oil, particularly heavy oil, exposed to WCS differentials has improved greatly over the past year with the upstart of Transmountain Pipeline expansion and of course the poor polls of Justin Trudeau’s government which appears to be path for a historic wipeout. Any LNG decisions in the coming months could further act as a positive catalyst for the energy space.

Mostly all Canadian heavy oil producers have responded favorably and received a strong response from public markets, with Strathcona still remaining as a lesser known for the reasons I will explain below, which I strongly believe offer new entrants and existing shareholders a significant opportunity.

Strathcona Resources (TSX: SCR)

Strathcona Resources was our top E&P idea for 2024 and has so far continued to outperform despite a pullback which was mostly sector based. In November 2023 we had it as a top idea that we thought could outperform even in a lower oil price scenario (see: 3 oil stocks that can outperform in a low commodity price environment), given its low multiple, extremely low liquidity, lesser known status with investors and substantial trading discount to peers. So far even after the run, those views haven’t changed although the valuation has made modest improvements.

High insider ownership is a current barrier for new entrants, but it won’t be forever

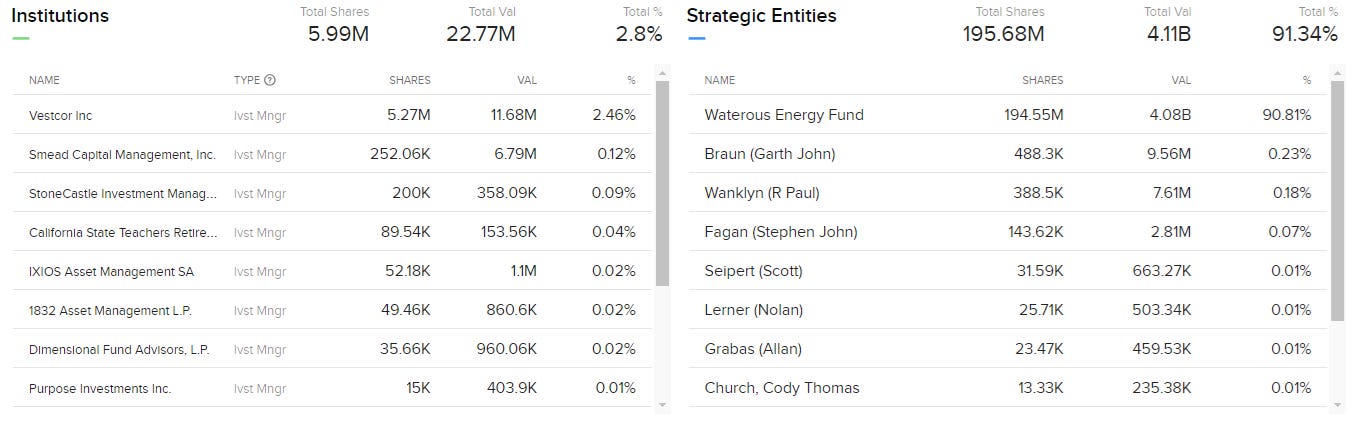

Strathcona Resources remains one of the least liquid names on the entire TSX, with the vast majority of the 214,235,608 shares held by Adam Waterous’ Waterous Energy Fund, with only 19.6 million available for any other parties. We estimate that only 3-4% of all shares are likely available for daily trading at most given the prior large Pipestone Energy ownership of GMT Capital and Riverstone assuming they did not sell near all-time lows after accepting the Strathcona shares in the Pipestone deal. Names with low liquidity tend to trade at lower multiples to peers, something we see could be a potential catalyst for the quarters ahead should liquidity improve.

Q1 conference call got us excited, direct shareholder returns are coming

On the Q1 2024 conference call (see audio link for Strathcona’s conference call) Strathcona management was asked by RBC analyst Rob Purdy about a capital return strategy and received a very clear and well thought out answer from Connor Waterous. Management sounded very confident that a base dividend was likely near, one that would be fulfillable at any point in the oil price cycle but management also expected that substantial amounts of free cash flow would be leftover. Further to Mr. Purdy’s point, he also asked whether an Imperial Oil-like substantial issuer bid would be an ideal way to enhance shareholder value and Strathcona management seems to feel like that would be a viable option as long as it enhanced value for investors.

Imperial Oil’s SIB/NCIB strategy has been one of the most successful on the TSX despite low liquidity, we see it as a comparable model for Strathcona Resources to pursue

Using Imperial Oil’s model as a possible example for Strathcona, we can see that it was unquestionably a roaring success. Imperial has been able to buy back around 27% of all shares outstanding since 2020 despite having Exxon Mobil as a majority investor holding approximately ~70% of all common shares outstanding. Slightly more liquid than Strathcona Resources in its current form but an adequate peer model. Using the use of renewed normal course issuer bids and substantial issuer bids plus a base dividend, Imperial Oil can comfortably claim the crown for the oilsands in being the company which has executed the best in shareholder returns via the buyback model.

Strathcona has a serious 2024/2025 organic expansion plan which will add shareholder value

With Transmountain Pipeline expansion online the risks of heavy oil blowouts has dissipated greatly in the near-term. While we think the WCS differentials may see pressure in the medium term if operators continue to ramp up, the ‘old fashion’ risk of total blowouts is far less than what it used to be as TMX opens up different end users on a global scale rather than be fully exposed to mostly US Midwest refineries, which sometimes have things like outages or prolonged workovers. Strathcona’s “in-house'“ supply chain with Montney assets offering the company an internal condensate (diluent) source for its heavier barrels can also serve as a hedge in cases with oil prices rise and C5+ differentials tightening, leading to improved economics that a pureplay SAGD operator would not have access to. If natural gas prices improve, Strathcona can also increase production on its Montney assets without taking on the sole risk that short cycle E&P’s are exposed to in commodity price downturns, as Strathcona will always have the support of low decline, low cost, heavy oil assets to back it up.

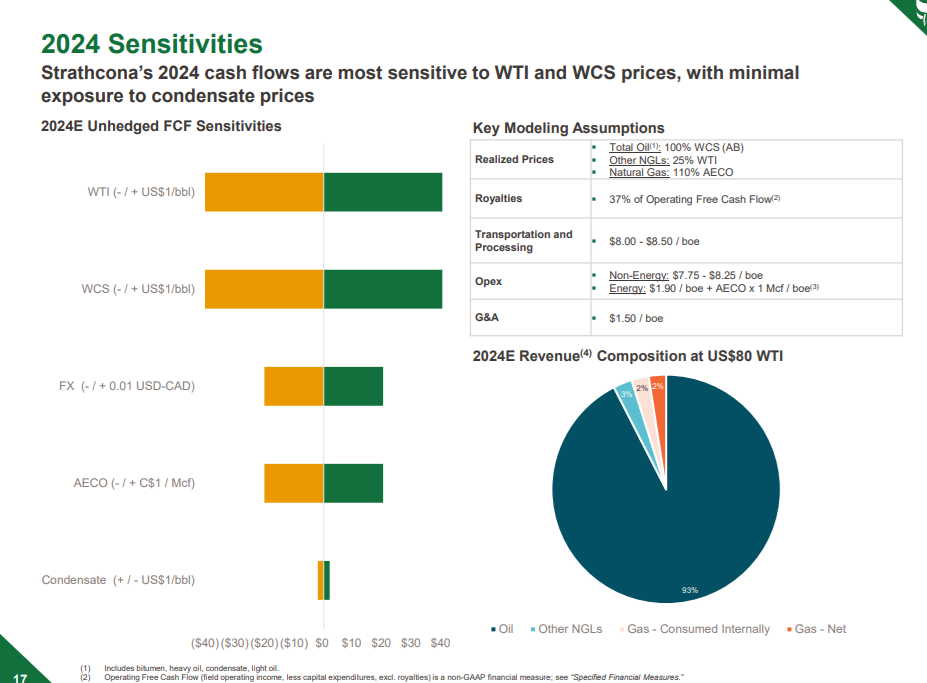

Strathcona Resources’ 2024 price sensitives are almost exclusively to oil and WCS differentials, which are within historical ranges. Natural gas is basically non-material here despite their Montney assets which themselves are liquids-rich, where natural gas is sold predominantly as a byproduct but does offer upside during periods of rising natural gas prices and should the AECO market once improve. The Montney assets which were acquired rather cheaply at a semi-cyclical trough may also potentially be spun off to other larger operators, in an improved natural gas environment as a number of E&P’s in the Alberta Montney are likely seeking to expand in the coming years. Overall we see Strathcona Resources in its current form as a heavy oil play with serious growth potential in 2024.

The near term catalyst is Strathcona’s capital return strategy which may come in Q2

The main catalyst can be depicted in the above slide from Strathcona’s latest presentation: the company continues to trade at a substantial multiple gap to peers despite having one of the lower risk profiles and best reserve profiles during a period where Canadian SAGD operators are being respected with lofty premiums relative to shorter cycle names by the public markets. The company is also one of the largest oil operators in the country, something we think will become impossible for public markets to ignore once liquidity structure improves. Strathcona should not be an exemption. The low liquidity issue with Waterous Energy Fund owning the bulwark presents opportunity to smaller retail investors. The potential for a near-term capital return plan which likely includes a base dividend plus a substantial issuer bid or the initiating of an NCIB feels like an extremely good risk-reward strategy for new investors, particularly after the latest pullback in both the stock and the commodity.

Thank you for reading and as always, if you have any questions or comments please leave them in the comment section.

Yours truly,

Roger Lafontaine

Partner, Head Trader & Research Analyst, Nugget Capital Partners

It seems like a strong narrative. Interesting asset base managed by a heavily invested and aligned management team. It appears from the conference call and analysts' comments that they will indeed declare an inaugural dividend. My only concern is that there isn't enough float for me to take a meaningful position.